ECB Press Conference: Lagarde speaks on policy outlook after holding key rates steady

Christine Lagarde, President of the European Central Bank (ECB), explains the ECB's decision to leave key rates unchanged at the April policy meeting and responds to questions from the press.

ECB press conference key quotes

"Economy was showing momentum before current turbulence."

"Domestic demand remains main driver of growth."

"Outlook highly uncertain."

"Incoming info suggests that conflict is weighing on activity."

"Business less confident about future."

"Supply chains coming under pressure."

"High energy to weigh on incomes."

"High energy costs to make firms, households reluctant to invest."

"Labour demand has cooled further."

"Households in solid financial position."

"Favourable starting point provides some cushioning."

"Fiscal responses should be temporary, targeted, tailored."

"Indicators of underlying inflation have changed little in recent months."

"Wage tracker indicates easing labour costs."

"Surveys indicate rise in other costs."

"Most measures of longer term inflation expectations stand around 2%."

"Increase in energy prices will keep inflation well above 2% in near term."

"Will closely monitor size and impact of energy price surge."

"Risks to growth are tilted to the downside."

"Worsening of global market sentiment could further dampen demand."

"Risks to inflation are tilted to the upside."

"Not going to say whether we're closer to any particular scenario."

"We are certainly moving away from baseline."

"To where exactly? I'm not sure is the most relevant assessment."

"Most critical is what impact energy prices will have."

"Made an informed decision of yet insufficient info."

"Debated at length various options."

"Decision was unanimous."

"Debated at length a hike."

"Some governors may argue both sides of proposals."

"Hard data is broadly in line with projections."

"There is such uncertainty, we need to revisit all issues at next meeting."

"Given position we're at, six weeks will be the right time to assess developments."

"Stagflation is a term better to be parked in the 1970s."

"We don't apply this term to circumstances today."

"Interest rates are the best tool that we can use."

"Reaction function has 3 anchors."

"Anchors are 2% target, symmetry, type of deviation from target."

"Will publish revised scenarios in June."

"Have abundance of liquidity."

"Did not discuss any new tools."

This section below was published at 12:15 GMT to cover the European Central Bank's policy announcements and the immediate market reaction.

The European Central Bank (ECB) announced on Thursday that it left key rates unchanged following the April policy meeting, as expected. With this decision, the interest rate on the main refinancing operations, the interest rates on the marginal lending facility and the deposit facility stood at 2.15%, 2.4% and 2%, respectively.

ECB policy statement key takeaways

"While incoming information has been broadly consistent with ecb’s previous assessment of inflation outlook, upside risks to inflation and downside risks to growth have intensified."

"ECB remains well positioned to navigate current uncertainty."

"ECB will closely monitor situation and follow a data-dependent and meeting-by-meeting approach to determining appropriate monetary policy stance."

"In particular, interest rate decisions will be based on its assessment of inflation outlook and risks surrounding it, in light of incoming economic and financial data, as well as dynamics of underlying inflation and strength of monetary policy transmission."

"ECB is not pre-committing to a particular rate path."

"APP and Pandemic Emergency Purchase Programme (PEPP) APP and PEPP portfolios are declining at a measured and predictable pace, as eurosystem no longer reinvests principal payments from maturing securities."

"War in the Middle East has led to a sharp increase in energy prices, pushing up inflation and weighing on economic sentiment."

"The longer the war continues and the longer energy prices remain high, the stronger is the likely impact on broader inflation and the economy."

"The Euro area entered this period of surging energy prices with inflation at around the 2% target, and the economy has shown resilience over recent quarters."

"Longer-term inflation expectations remain well anchored, although inflation expectations over shorter horizons have moved up significantly."

"Implications of the war for medium-term inflation and economic activity will depend on the intensity and duration of the energy price shock and the scale of its indirect and second-round effects."

"The implications of the war for medium-term inflation and economic activity will depend on the intensity and duration of the energy price shock and the scale of its indirect and second-round effects."

"The Governing Council is committed to setting monetary policy to ensure that inflation stabilises at the 2% target in the medium term."

"Governing Council will closely monitor the situation and follow a data-dependent and meeting-by-meeting approach to determining the appropriate monetary policy stance."

Market reaction to ECB rate decision

EUR/USD retreated slightly from session highs with the immediate reaction to the ECB policy announcement and was last seen trading at 1.1695, rising 0.17% on the day.

Euro Price Today

The table below shows the percentage change of Euro (EUR) against listed major currencies today. Euro was the strongest against the US Dollar.

| USD | EUR | GBP | JPY | CAD | AUD | NZD | CHF | |

|---|---|---|---|---|---|---|---|---|

| USD | -0.13% | -0.22% | -2.38% | -0.10% | -0.43% | -0.59% | -0.79% | |

| EUR | 0.13% | -0.05% | -2.25% | 0.03% | -0.28% | -0.38% | -0.64% | |

| GBP | 0.22% | 0.05% | -2.22% | 0.09% | -0.22% | -0.37% | -0.58% | |

| JPY | 2.38% | 2.25% | 2.22% | 2.32% | 2.00% | 1.78% | 1.59% | |

| CAD | 0.10% | -0.03% | -0.09% | -2.32% | -0.33% | -0.51% | -0.70% | |

| AUD | 0.43% | 0.28% | 0.22% | -2.00% | 0.33% | -0.15% | -0.36% | |

| NZD | 0.59% | 0.38% | 0.37% | -1.78% | 0.51% | 0.15% | -0.20% | |

| CHF | 0.79% | 0.64% | 0.58% | -1.59% | 0.70% | 0.36% | 0.20% |

The heat map shows percentage changes of major currencies against each other. The base currency is picked from the left column, while the quote currency is picked from the top row. For example, if you pick the Euro from the left column and move along the horizontal line to the US Dollar, the percentage change displayed in the box will represent EUR (base)/USD (quote).

This section below was published as a preview of the European Central Bank's monetary policy decisions at 05:00 GMT.

- The European Central Bank is expected to maintain its current interest rate policy.

- Markets to focus on signals regarding a possible rate hike as early as June.

- The energy shock due to the Middle East war is fuelling inflationary risks whilst weighing on growth.

The European Central Bank (ECB) is scheduled to announce its monetary policy decision on Thursday, following its April meeting. The Frankfurt-based institution is widely expected to keep its key interest rates unchanged, leaving the deposit facility at 2%, a level considered broadly neutral. Recent communications from policymakers, including ECB President Christine Lagarde, suggest that the Governing Council prefers to wait for more data before taking action, particularly given the high uncertainty surrounding the Middle East war and its impact on energy prices.

Christine Lagarde is due to hold a press conference after the decision, which will be closely scrutinized for clues about the policy outlook. Questions are likely to focus on the persistence of the energy shock, the risk of second-round effects on inflation, and the growing signs of a slowdown in economic activity across the Eurozone. The central bank is expected to reiterate its data-dependent and meeting-by-meeting approach, while keeping all options open.

What to expect from the ECB interest rate decision?

The ECB faces an increasingly complex macroeconomic backdrop characterized by a stagflationary shock. On the one hand, rising energy prices linked to geopolitical tensions are pushing headline inflation higher. On the other hand, underlying inflation remains more contained, while forward-looking indicators, such as the Purchasing Managers Index (PMI) surveys, signal a deterioration in economic activity, particularly in the services sector, which fell to 47.4 in April.

The central bank is likely to keep rates unchanged as it awaits greater clarity, but the risk of a June hike is increasing, several analysts note, especially if disruptions in energy supply persist. Deutsche Bank highlights that policymakers are dealing with “double uncertainty” related to both the evolution of the Middle East conflict and the transmission of higher energy prices into broader inflation.

Recent economic data illustrate this dilemma. Headline inflation has risen due to energy costs, while core inflation has edged lower, suggesting limited immediate spillover effects. However, survey figures indicate rising input costs and selling prices, pointing to potential second-round effects. At the same time, growth indicators have weakened, with PMIs slipping into contraction territory and consumer confidence deteriorating.

In this context, the ECB is expected to maintain its “graduated reaction function,” ranging from looking through temporary shocks to implementing measured or more forceful tightening if inflation proves persistent. Most analysts see April as too soon to act, but the central bank will likely preserve a hawkish bias to keep inflation expectations anchored.

Communication will therefore be key. Policymakers are expected to emphasize elevated uncertainty, reaffirm their commitment to price stability, and stress policy optionality. As noted by several institutions, the ECB is likely to adopt a “hawkish hold,” signaling readiness to act without pre-committing to a specific path.

How could the ECB meeting impact EUR/USD?

Ahead of the announcement, markets are largely pricing in a cautious ECB stance but maintaining expectations of policy tightening later this year.

In the near term, the central bank’s impact on the pair may be limited unless it delivers a significant surprise. A clearly hawkish tone, reinforcing expectations of a June rate hike, could support the Euro (EUR) by pushing short-term rate differentials in its favor. Conversely, a more cautious sta

nce or dovish communication could weigh on the common currency, particularly if growth concerns dominate the narrative.

Market pricing currently reflects expectations of around two rate hikes this year. Around 65 basis points of cumulative tightening are priced in by year-end, with a first move likely in June, according to Danske Bank, while ING notes that markets remain firmly anchored around a June liftoff scenario despite the ECB’s cautious stance. Therefore, the key for traders will be how strongly President Lagarde signals the likelihood of such a move. Any indication that second-round inflation effects are building could strengthen the case for tightening and provide support to the Euro.

However, external factors remain crucial. Oil prices, geopolitical developments, and global risk appetite continue to play a dominant role in EUR/USD dynamics. As a result, unless the ECB significantly shifts market expectations, the pair may remain primarily driven by broader macro forces rather than the policy decision alone.

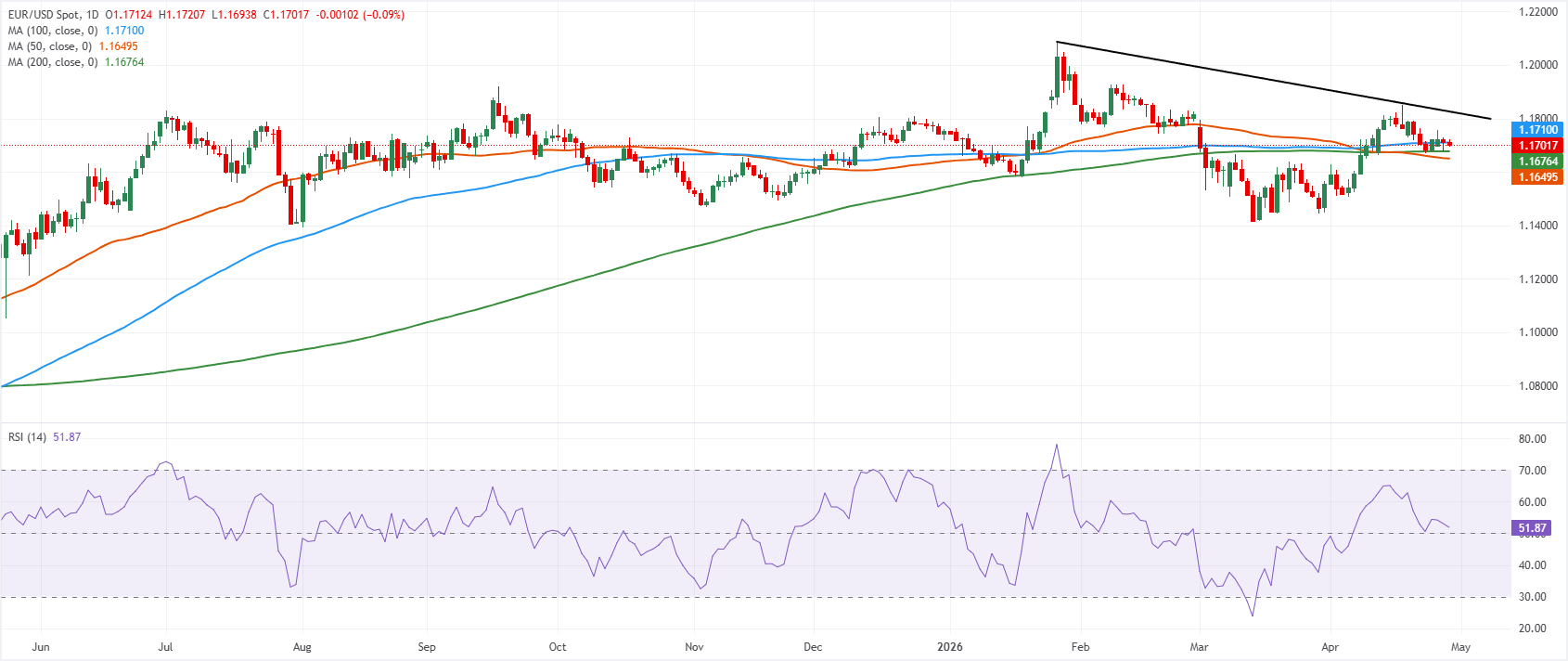

Since early June 2025, the EUR/USD pair has been trading within a broad horizontal range, with no clear trend. In the daily chart, the pair sits just under the 100-day Simple Moving Average (SMA) at 1.1710 while holding above the 200-day SMA at 1.1676 and the 50-day SMA at 1.1650, leaving the near-term tone broadly neutral with a slight constructive bias as long as these underlying averages hold. The Relative Strength Index (RSI) has eased back toward the low-50s, hinting at waning upside momentum after the recent recovery but not yet signalling overbought or oversold conditions.

On the topside, immediate resistance emerges at the 100-day SMA around 1.1710, with a more significant cap aligned with the downward resistance trend line near 1.1823, where the broader corrective structure would be challenged. On the downside, initial support is seen around the 200-day SMA at 1.1676, ahead of the 50-day SMA near 1.1650, where a break would likely expose a deeper pullback and undermine the current mild bullish bias.

ECB FAQs

The European Central Bank (ECB) in Frankfurt, Germany, is the reserve bank for the Eurozone. The ECB sets interest rates and manages monetary policy for the region. The ECB primary mandate is to maintain price stability, which means keeping inflation at around 2%. Its primary tool for achieving this is by raising or lowering interest rates. Relatively high interest rates will usually result in a stronger Euro and vice versa. The ECB Governing Council makes monetary policy decisions at meetings held eight times a year. Decisions are made by heads of the Eurozone national banks and six permanent members, including the President of the ECB, Christine Lagarde.

In extreme situations, the European Central Bank can enact a policy tool called Quantitative Easing. QE is the process by which the ECB prints Euros and uses them to buy assets – usually government or corporate bonds – from banks and other financial institutions. QE usually results in a weaker Euro. QE is a last resort when simply lowering interest rates is unlikely to achieve the objective of price stability. The ECB used it during the Great Financial Crisis in 2009-11, in 2015 when inflation remained stubbornly low, as well as during the covid pandemic.

Quantitative tightening (QT) is the reverse of QE. It is undertaken after QE when an economic recovery is underway and inflation starts rising. Whilst in QE the European Central Bank (ECB) purchases government and corporate bonds from financial institutions to provide them with liquidity, in QT the ECB stops buying more bonds, and stops reinvesting the principal maturing on the bonds it already holds. It is usually positive (or bullish) for the Euro.

Economic Indicator

ECB Press Conference

Following the European Central Bank’s (ECB) economic policy decision, the ECB President gives a press conference regarding monetary policy. The president’s comments may influence the volatility of the Euro (EUR) and determine a short-term positive or negative trend. If the president adopts a hawkish tone it is considered bullish for the EUR, whereas if the tone is dovish the result is usually bearish for the Euro.

Read more.Next release: Thu Apr 30, 2026 12:45

Frequency: Irregular

Consensus: -

Previous: -

Source: European Central Bank